Silicon Valley Bank Is the 2nd Largest Bank Failure

It will take some time, but the FDIC was designed for moments like this

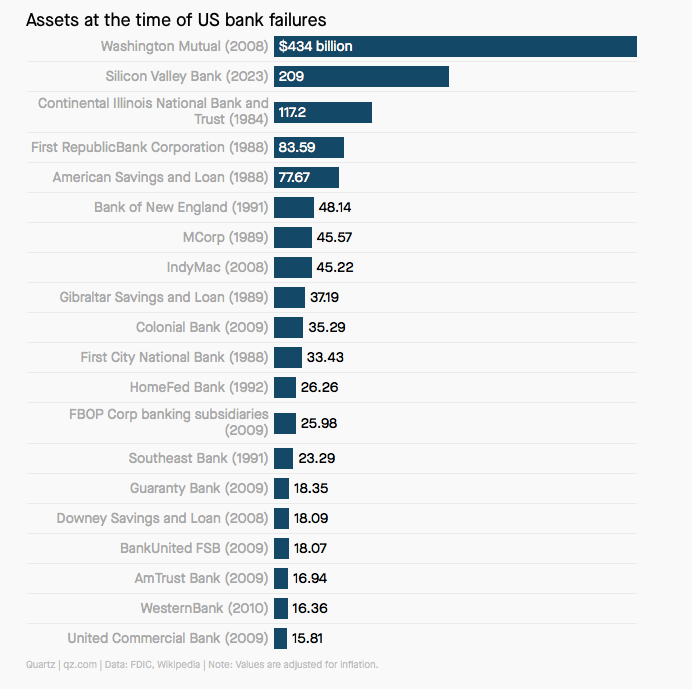

The FDIC-seizure of Silicon Valley Bank is the second-largest US bank failure in history as it held $209 billion in assets at the time of its collapse. Even after adjusting for inflation, by assets it trails only Washington Mutual, which held $434 billion in assets when it failed in 2008.

The Silicon Valley Bank failure rocked the tech industry and sent tremors throughout Wall Street as it largely serves start-ups and venture capitalists. Those with deposits at the bank – namely start-up founders and venture capitalists – worried that money needed to pay employees is frozen or worse, lost.

And while the failure of Silicon Valley Bank is troubling, given their unusual deposit-base and unique shortcomings, it is unlikely that we will see a run of bank failures any time soon. But did you know that bank failures and collapses have been a part of the financial landscape for centuries? It’s true.

In fact, it is not at all unusual for at least a few U.S. banks to fail in any given year – it’s just been more than 2 years as the last time a bank backed by the FDIC failed was October 23, 2020 when Almena state Bank closed. This is not to say that Silicon Valley Bank’s failure should be dismissed as inconsequential at all, because its failure will continue to ripple through the banking system and through Wall Street for some time. But it’s also important to maintain perspective.

The FDIC

Throughout history, there have been numerous instances of banks that were unable to meet their financial obligations, resulting in the loss of depositor's money. In the United States, the Federal Deposit Insurance Corporation (FDIC) was created in response to the Great Depression of the 1930s, which saw the failure of over 9,000 banks.

The FDIC is an independent agency of the federal government that provides insurance to depositors in case their bank fails. The creation of the FDIC was a direct response to the widespread bank failures that occurred during the Great Depression. In those days, depositors had no protection, and if their bank failed, they stood to lose all their savings. The FDIC was created to restore confidence in the banking system and to provide a safety net for depositors.

The FDIC is funded by premiums paid by member banks, and it guarantees deposits up to a certain amount. The current limit is $250,000 per depositor, per insured bank. This means that if a bank fails, the FDIC will step in and ensure that depositors get their money back, up to the insurance limit.

Since its creation in 1933, the FDIC has played a vital role in maintaining stability in the banking system. It has insured trillions of dollars in deposits and has helped to prevent bank runs and panics. While there have been bank failures since the FDIC's creation, the number has been significantly lower than before.

The Largest Bank Failure

One of the most notable bank failures in recent history was the collapse of Washington Mutual in 2008. At the time, it was the largest bank failure in U.S. history, with over $300 billion in assets. The failure was due in large part to the bank's exposure to the subprime mortgage market. When the housing market crashed, Washington Mutual was left with a large number of bad loans, and it was unable to meet its financial obligations.

The FDIC stepped in and seized the bank, ensuring that depositors got their money back up to their guaranteed amount. While the failure was a significant event, the FDIC's insurance helped to prevent it from turning into a larger financial crisis.

Again, while it’s never comfortable, especially for those with assets at a failed bank, bank failures and collapses have been a part of the financial landscape for centuries. But the FDIC plays a vital role in maintaining stability in the banking system as its insurance provides a safety net for depositors, ensuring that they get their money back up to the applicable limits, if their bank fails. As a depositor, it's important to understand the limits of FDIC insurance and to choose a bank that is FDIC-insured.

Important Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This article was prepared by FMeX.

LPL Tracking #1-05363671